This project was moved on HOLD with PROBLEM status! Wait for further updates…

Recently you could read the EN “First Thoughts” article for Stoqman platform, where we showed investment plans offered by it to all participants and potential investors. Let’s refresh a few things in mind:

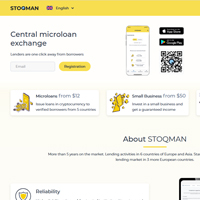

This platform offers 3 different groups of investment plans for you and other investors. Let’s take a look:

Microloans – 0.9%-1.5% every 24 hours for 4-21 days (min. deposit $12, Profit – up to 31.5%) Deposit Back at the end of the term.

Small Business – 0.8%-1.1% every 24 hours for 12-24 days (min. deposit $50, Profit – up to 26.4%) Deposit Back by Equal installments every 6 days.

Company development – 1.1%-1.9% every 48-72 hours for 30-180 days (min. deposit $500, Profit – up to 342%) Deposit Back at the end of the term.

As you can see these plans have a difference in accrual period as well as the way of returning back your initial deposit. There are few more details we will have to take into account when reviewing them. At the same time such plans are designed to be attractive as much as possible for both camps of investors (adventurous and conservative).

From here we need to continue and to do our usual math.

*Please note that all of these investment plans are divided into subcategories depending of deposit amount, that is why you can see the range of days (investment period) and range of profit on each them. You can check your internal account on Stoqman to better understand all of the ranges..

Let’s take Small Business plan as our example.. Here we take the max. allowed period of days. In fact some investors can possibly choose different (less) plan’s timeframe with less profit accordingly.

No conversion factor of 30/22 (calendar days/business days) needed – the plan works everyday without days off.

Stoqman offers investors 1.1% / per day interest rate for 24 days. Principal is back AND as a notable feature – your principal will be back to you with Equal installments every 6 days, during your plan. So after 6 days you will already receive back a part of your initial deposit.

Let’s check a break even point. With this (Equal installments every 6 days) feature you may get it a bit before the end of your plan.. But mainly the thing remains the same as for Principal Back plans – the break even point is at the END of your term. Your Net Profit will be 26.4% (1.1% X 24 days).

Total Gross Interest is around 126.4% (Net Profit + Principal Back).

Now we check this plan thorough the DNI (Daily Net Interest) filter to see more details..

*Read EN HYIP Insights article #12 Part 3 and Part 4, to understand what is a DNI (Daily Net Interest)..

As it usually happens with Principal Back plans the DNI is equal to daily profit: Let’s see – We divide our Net Profit (26.4%) by 24 days and get 1.1% of DNI level. We consider it as a MEDIUM interest plan, thus it can attract both adventurous and conservative investors, who can participate in this OR in other two plans which are also quite affordable for a big part of investors..

If necessary, in one of the future articles, we will analyze in detail another plan for this program. Some investors may need this...

In Part 2 of the Review we will pay attention to additional information which will be useful for you, regardless of whether you joined Stoqman or still thinking and waiting for the right moment.. Please stand by..

*********************************

If one of the paying programs on our Monitor appeals to you, please support EmilyNews by registering for it on our website. Thanks very very much!

EN web Support Chat | Hyips and Crypto questions – HyipChatEN

Telegram Chat for Crypto and Hyip reports: @HyipChatEN

*********************************

Be the first to get most important HYIP news everyday!

Simply Follow EN Facebook, EN Telegram, EN Twitter

or Subscribe to EN Feedburner and submit your email address!

If you like this article and want to support EN – please share it by using at least few of social media buttons below. Thanks and See you tomorrow!